New pensions reforms have seen an overall shift from those who once would automatically buy an annuity to now considering income drawdown. Purchasing an annuity was a relatively straight forward process, simply selecting the provider who were offering the most income. Income drawdown is not as simple however, there are a number of factors which will determine the decision.

Income drawdown is a complex product which involves investment risk and needs planning. It is key to understand what’s involved and what considerations you should have before selecting a provider as there are a few moving parts.

1.The income you require

As you move through retirement the need for income may change. A common pattern is to spend more money in the early years when you have the desire and health but less in middle retirement. Later retirement may require an increase availability of funds for care home cost. Cash flow forecasting is a useful way of totting up your assets and working out what the likely need for expenditure will be. We like the useful planning and free tool from RetireEasy.

2.Investment growth

As the majority of the drawdown plan will stay invested, the performance and growth will change on a daily basis. It isn’t as easy therefore to forecast annual returns. The solution is to pick a number of investment funds which meet your attitude to investment risk. This should provide a level of volatility which you can tolerate.

As a general rule of thumb, the higher the risk, the wider the fluctuations both positive and negative.

As a general rule of thumb, the higher the risk, the wider the fluctuations both positive and negative.

This graph from Investorbee gives a good example of this.

3.Inflation

The rising cost of living through retirement will reduce the spending power of the money you take. Most annuities pay a level income and therefore there isn’t an option to take more income if the cost of living increases, you simply have to budget better. Income drawdown will let you take more to compensate for rising prices. Sustainability of your fund is therefore of the upmost importance and regular review and a check on the impact of withdrawals should be carried out each year.

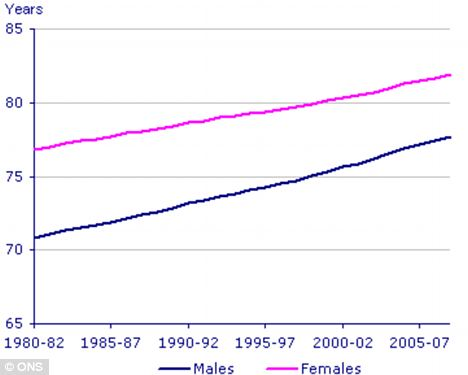

4.Date of death

Unfortunately, we can’t forecast the date we’ll get a knock on the door from the grim reaper. We

therefore need to keep enough funds should we live longer than expected. With medical advances, the average age of death in both men and women continues to increase.

therefore need to keep enough funds should we live longer than expected. With medical advances, the average age of death in both men and women continues to increase.

With this in mind we need to budget the amount of money we take, forecast inflation, investment growth rates and predict our date of death if we want a comfortable retirement. Quite a task you’ll agree.

So how does this relate to the drawdown provider you chose?

The drawdown provider you chose and how you chose it will have an impact on the feasibility you can correctly navigate the above.

Your needs

The different drawdown providers have plans which will cater for different needs. Think about it like buying a car. Do you just want to go from A to B and are not bother how you get there or do you want the ability to have all the extras like how fast you’re going, how much fuel your using, estimated time of arrival, after sales service, reliability, option to

change models if you don’t like your ride etc. Well drawdown plans cater for a similar group of needs.

If you just want to take advantage of what drawdown allows you to do (access all your money), there are providers and plans to suit your needs. The straight from A to B with no fuss option will often restrict access to a wider variety of funds but will be low cost to run. You probably won’t find you’re in top performing funds or be allowed to take advantage of a specific sector which might be growing, but you’ll be allowed to take all you funds out when you want according to drawdown rules.

This no frills, often referred to as low-cost option is surprisingly popular. Many companies offer a low-cost option alongside their more established proposition as it is expected that a large proportion of people moving into drawdown post-April 2015 won’t need or want a more complex plan.

Choice of investments

For those that want a little more than a low cost A to B option and want the comfort, flexibility and service of the equivalent of buying a new car from a with bells and whistles there are a variety of options.

There are up to 8000 funds accessible through drawdown providers. A portfolio can be constructed to suit virtually everyone’s  requirements. There are funds available for every sector, assets class, geographical region and risk level. The hard part is to narrow these down to something that suits your needs.

requirements. There are funds available for every sector, assets class, geographical region and risk level. The hard part is to narrow these down to something that suits your needs.

We recommend using a qualified financial adviser for this. They can correctly assess your needs and build a tailored portfolio for you. If you want the Rolls Royce of service they may outsource this to a Discretionary Fund Manager (DFM). DFM’s cost a little more in annual charges but you get more of a personal service.

Many financial advisers have in-house, brand labelled portfolios which have been pre-constructed. This is where they have already grouped a number of funds into risk levels. These might be from risk level 1 to 10 and consist of 10 to 20 separate funds. The advantage of this being that all the hard work of researching the whole investment fund market has already been done for you.

If you want to self-manage your drawdown investment, many of the providers have a suggested portfolio, again pre-selected and labelled into a certain risk category. The larger drawdown providers have in-house research teams which may be one reason to select one of these companies above another.

Quantity of fund access isn’t a sole reason to choose a provider however. The second main consideration is

Cost

One of the main problems of the drawdown and investment platform industry is the disparity in how they all charge for their services. There is no set formula or guideline to follow. This makes calculating the cost of one provider to another very difficult. Providers might charge annual admin fees, annual income withdrawal fee’s, fund switch fee’s, switching in fee’s, fee’s dependant on assets held and different provider may charge a different annual management change for the same fund. On top of this some providers have discounts on fund fees depending on assets held. Add onto this an annual cost if you are taking ongoing financial advice and it became somewhat confusing.

A lower cost provider will often be so for a reason. They might offer access to a lower amount of funds or not provide as many tools as a provider who charges slightly more. The more established providers may charge slightly more but offer a greater degree of financial security and may have a bigger in-house research team meaning funds or portfolios could be expected to perform better.

In summary

The two main considerations when comparing one provider to another are ongoing costs and confidence in fund management. If you’re picking in-house funds you can research the performance of these on sites such as http://www.trustnet.com/. If you’re using a financial adviser they will be able to give you the performance of a recommended portfolio.

You should have a good idea of your income needs per year and if not you should complete an income to outgoings exercise. Planning is everything with income drawdown. Do it right and it can benefit you and your family, do it wrong and it’s going to impact your standard of living in later retirement.

[…] was the best option, drawdown is a little more opaque. Those looking to enter drawdown need to prioritise costs, fund access, portfolio design, performance and usability in order to find a provider which suits them. Blackrock entering the market gives them one more […]