Emergency Tax on Pension Withdrawals: How to Reclaim What You're Owed

HMRC applies emergency tax codes to first pension withdrawals, often deducting thousands more than you owe. Learn how to use forms P55, P53Z, and P50Z to reclaim overpaid tax — and why this matters especially before 5 April.

When you make your first flexible withdrawal from a defined contribution pension, there's a very common and frustrating surprise waiting: HMRC applies an emergency tax code to your payment. The result? You may end up paying far more income tax than you actually owe — sometimes thousands of pounds more. The good news is that you can claim it back. Here's everything you need to know.

Why Does HMRC Apply Emergency Tax to Pension Withdrawals?

Under the pension freedoms introduced in April 2015, people aged 55 and over (rising to 57 from 2028) can access their defined contribution pension flexibly. However, HMRC's PAYE system was designed long before pension freedoms existed, and it has a quirk that catches many people off guard.

When your pension provider makes your first flexible payment, it typically doesn't have a current tax code for you. In this situation, HMRC instructs providers to apply an emergency tax code — usually the basic rate on a Month 1 basis (also known as a "Week 1/Month 1" code).

This approach assumes that the single withdrawal you're taking is the first instalment of many equal payments across the tax year. For example, if you take a lump sum of £30,000, the emergency code may treat this as if you're earning £360,000 a year — triggering the highest income tax rates on a large portion of your withdrawal.

Many people consider this one of the most poorly understood aspects of pension drawdown, and it has led to HMRC refunding hundreds of millions of pounds in overpaid tax since 2015.

How Much Tax Could You Overpay?

The overpayment can be significant. Figures from HMRC consistently show that billions of pounds in overpaid pension tax have been reclaimed since pension freedoms were introduced. In Q1 2024 alone, HMRC refunded over £46 million to people who had been emergency taxed on pension withdrawals.

To illustrate the potential impact, consider a simplified example:

- You take a one-off lump sum of £20,000 from your pension (on top of your tax-free cash)

- Your actual income tax liability might be £2,000 if this is your only income and you have a full personal allowance (£12,570 for 2025/26)

- But under the emergency tax code (Month 1 basis), your provider might deduct £5,000 or more

- This means you could be owed a refund of approximately £3,000

The actual figures depend on your individual circumstances, the size of the withdrawal, and what other income you receive. Consulting a qualified financial adviser before taking pension withdrawals is always recommended to understand the likely tax treatment.

What Forms Do You Need to Claim Your Refund?

HMRC provides specific reclaim forms depending on your situation. You do not need to wait until the end of the tax year — you can claim in-year as soon as the withdrawal has been made and you know your circumstances for the rest of the tax year.

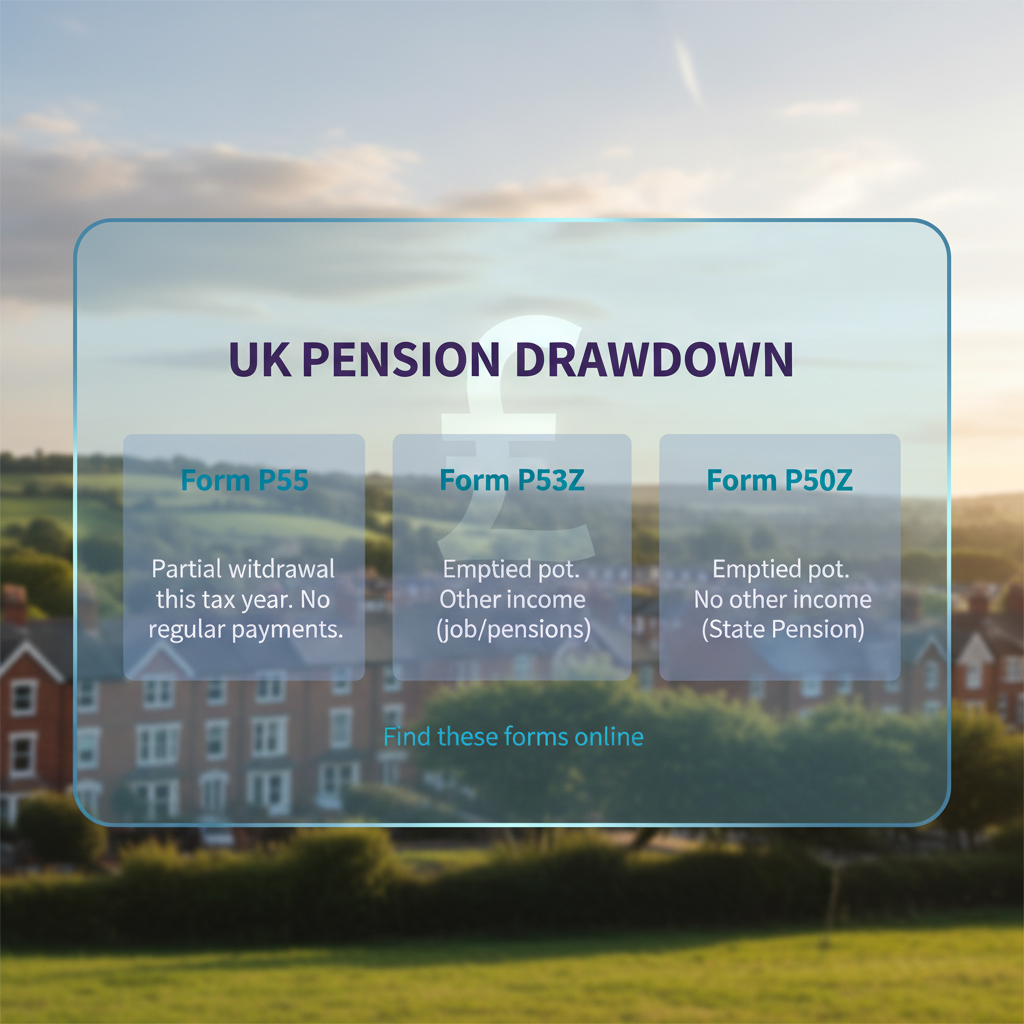

Form P55 — Partial Pension Withdrawal (Not Your Full Fund)

Use Form P55 if:

- You've taken a partial (flexible) withdrawal — not the whole fund

- You do not plan to take any further flexible payments in the current tax year

- Your provider has already taxed your payment and issued a PAYE deductions certificate (P45)

Form P55 is available on GOV.UK and can be submitted online or by post. HMRC typically processes in-year reclaims within 3-4 weeks.

Form P53Z — Taken Your Entire Pension Pot (With Other Income)

Use Form P53Z if:

- You've taken your entire pension fund as a lump sum (fully encashed)

- You have other sources of income in the same tax year (such as employment, state pension, or other pensions)

Form P50Z — Taken Your Entire Pension Pot (No Other Income)

Use Form P50Z if:

- You've taken your entire pension fund as a lump sum

- You have no other income in the same tax year

- You have stopped work and have no plans to work again in the tax year

Self-Assessment Tax Return

If you complete an annual Self-Assessment tax return, you can also reclaim overpaid pension tax through this route at the end of the tax year. However, in-year reclaims via the forms above are generally much faster if you're confident about your income position for the year.

What If You Take Multiple Drawdown Payments Throughout the Year?

If you plan to take regular drawdown payments (monthly, quarterly, or ad hoc), the emergency tax situation resolves itself more quickly. Once your pension provider has a current tax code from HMRC (usually after your first payment), subsequent payments should be taxed more accurately.

However, many people consider consulting a financial adviser before taking any drawdown payments to ensure the withdrawals are structured in the most tax-efficient way. Timing, amount, and frequency can all affect your overall tax position significantly.

What Is the Tax-Free Cash Component?

It's important to understand that not all pension withdrawals are taxable. When you access a defined contribution pension, you are typically entitled to take up to 25% of your fund as a Pension Commencement Lump Sum (PCLS) — commonly known as tax-free cash. This portion is not subject to income tax.

Emergency tax codes should only apply to the taxable portion of your withdrawal (the remaining 75%). However, errors can occur, and it's worth checking your pension provider's payment breakdown carefully.

Does This Affect UFPLS Withdrawals Too?

Yes. If you take an Uncrystallised Funds Pension Lump Sum (UFPLS) — where 25% is paid tax-free and 75% is taxed at the point of withdrawal — emergency tax codes apply in exactly the same way. The 75% taxable portion will be subject to the Month 1 emergency tax code if it's your first flexible access of that pension.

This is one reason many financial advisers suggest that taking a small initial drawdown (to "trigger" the correct tax code from HMRC) before making larger withdrawals may be worth considering. However, this is a personal decision that depends on your individual circumstances — professional advice is strongly recommended.

Key Deadlines to Be Aware Of

The UK tax year runs from 6 April to 5 April. In-year reclaim forms (P55, P53Z, P50Z) can only be used to reclaim tax within the same tax year the withdrawal was made.

If the tax year has ended before you submit your reclaim, you'll need to either:

- Complete a Self-Assessment tax return (if you're registered for Self-Assessment)

- Contact HMRC directly to request a PAYE repayment for the previous tax year

With the 2025/26 tax year ending on 5 April 2026, anyone who has made a first pension withdrawal this tax year and believes they've been emergency taxed should consider acting promptly to reclaim before the year-end deadline passes.

How to Submit Your Reclaim

All three reclaim forms are available on GOV.UK. Options to submit include:

- Online via your Personal Tax Account (fastest route)

- Post to the HMRC PAYE address shown on the form

You'll need to have the following to hand:

- Your National Insurance number

- Your pension provider's PAYE reference (found on your payslip or P45/P60)

- Details of the withdrawal amount and tax deducted

- Details of any other income sources in the tax year

Common Questions About Pension Emergency Tax

Will HMRC automatically refund the overpayment?

Not automatically in-year. HMRC may make automatic adjustments at the end of the tax year as part of PAYE reconciliation, but this process can take months. Submitting an in-year reclaim form is the fastest way to get your money back.

Can my pension provider sort this out for me?

Your provider will tax your withdrawal at the code HMRC instructs them to use. They cannot change this code themselves. Once they receive an updated code from HMRC (triggered by your submission of a reclaim form or by HMRC's own reconciliation), future payments will be adjusted. But overpaid tax from previous payments needs to be reclaimed via HMRC directly.

Is this the same as a tax rebate?

It's similar in effect — you're reclaiming income tax that was deducted at source. The forms are specific to pension overpayments, so use the correct one (P55, P53Z, or P50Z) rather than a general tax reclaim form.

How long does it take to get the refund?

HMRC typically aims to process in-year pension reclaim forms within 3-4 weeks. During busy periods (particularly around tax year end), this may take longer. Online submissions are generally processed faster than postal ones.

How a Financial Adviser Can Help

Emergency tax on pension withdrawals is just one of many tax considerations that many people find valuable to explore with a qualified financial adviser before accessing their pension. An adviser can help you:

- Understand how different withdrawal methods (drawdown, UFPLS, annuity) are taxed

- Plan the timing of withdrawals across tax years to minimise your overall tax liability

- Coordinate pension income with state pension, ISAs, and other assets

- Understand the Money Purchase Annual Allowance (MPAA) — triggered by your first flexible access

- Ensure your nominations and death benefit arrangements are up to date

Taking pension money might seem straightforward, but the interaction with income tax, MPAA, and state benefits can be complex. Planning ahead typically makes a significant difference to outcomes over the long term.

Speak to a qualified financial adviser for personal guidance on pension withdrawals and tax planning. The information on this page is educational and does not constitute financial advice. Tax rules may change, and your personal circumstances will affect the tax treatment of any pension withdrawal.

Further reading: Emergency Tax on Pension Drawdown: How to Avoid It and Reclaim What You're Owed

One of the most frustrating — and surprisingly common — surprises for people taking money from their pension is receiving far less than they expected. The culprit is usually emergency tax on pension drawdown.

HMRC applies emergency tax when you make your first flexible withdrawal from a pension pot. In many cases, this results in a tax deduction that's two or three times higher than it should be — sometimes leaving people short by thousands of pounds. The good news is that you can reclaim it, often quickly. This article explains exactly how emergency tax works, why it happens, and which HMRC form to use to get your money back.

Why Does HMRC Apply Emergency Tax on Pension Withdrawals?

When you take a flexible pension withdrawal for the first time, your pension provider doesn't usually hold an up-to-date tax code for you. Without a valid tax code, HMRC instructs them to use an emergency tax code — typically Month 1 basis (also shown as "M1" or "W1" on your payslip).

The problem is that Month 1 basis assumes you'll take the same amount every month for the rest of the tax year. So if you take a lump sum of £20,000 in one go, HMRC effectively assumes you'll earn £20,000 × 12 = £240,000 that year — and taxes your withdrawal accordingly. At that income level, much of it falls into the 40% or even 45% tax band, even if your actual annual income is far lower.

How Much Tax Could You Overpay?

The overpayment varies depending on your total income and the size of your withdrawal, but it's common for first-time drawdown users to overpay between £1,000 and £8,000 in tax on a single withdrawal.

Here's a simplified illustration of the scale of overpayment:

| Withdrawal Amount | Emergency Tax (approx) | Correct Tax (no other income) | Overpayment |

|---|---|---|---|

| £10,000 | ~£3,200 | ~£0 (within personal allowance) | ~£3,200 |

| £20,000 | ~£6,900 | ~£1,486 | ~£5,400 |

| £30,000 | ~£11,200 | ~£3,486 | ~£7,700 |

| £50,000 | ~£20,000 | ~£9,432 | ~£10,600 |

Figures are illustrative for 2025/26. Assume no other income in the tax year. Your circumstances will vary.

The Three HMRC Reclaim Forms

HMRC provides three different forms to reclaim overpaid pension tax. The correct form depends on whether you've taken all the money from your pension pot or just part of it.

P55 — Partial Withdrawal

Use Form P55 if you have taken a partial withdrawal from your pension pot and the pension pot has not been fully emptied. This is the most common scenario for drawdown users who take a lump sum while leaving the rest invested.

- Eligibility: You haven't taken all your pension savings from this provider

- Not eligible if: Your pension provider is using a cumulative tax code (meaning they've already corrected your tax)

- Download: HMRC P55 form

P53Z — Full Withdrawal and You Have Other Income

Use Form P53Z if you have emptied your pension pot in one go (taken everything as a lump sum) and you have other income in the same tax year (such as employment, State Pension, or other pensions).

- Eligibility: You've taken the full pension pot, and you have other taxable income

- Download: HMRC P53Z form

P50Z — Full Withdrawal and No Other Income

Use Form P50Z if you have emptied your pension pot and you have no other income in the tax year — you've stopped working and this pension payment is your only income.

- Eligibility: You've taken the full pension pot, and you have no other taxable income this tax year

- Download: HMRC P50Z form

→ Still money left in the pot? Use P55

→ Emptied the pot + have other income? Use P53Z

→ Emptied the pot + no other income? Use P50Z

How to Complete and Submit the Form

All three forms can be completed online via the GOV.UK website, or downloaded and posted to HMRC. The online route is significantly faster.

You'll need the following information before you start:

- Your National Insurance number

- The amount you withdrew from your pension

- The amount of tax deducted (shown on your pension provider's payment advice or P45)

- Your pension provider's name and address

- Details of any other income in the tax year (employment, other pensions, State Pension)

- Your bank details for the refund

Once submitted online, HMRC typically processes refunds within 4–6 weeks, though many people report receiving money back within 2–3 weeks. Postal submissions take longer — allow 8–12 weeks.

Can You Avoid Emergency Tax Altogether?

In some cases, yes — though it depends on your pension provider and circumstances.

Take a Small Initial Withdrawal First

Some providers will issue you an updated tax code after your first (even small) withdrawal. If you take a minimal initial withdrawal — say £1 — your provider may receive a new tax code from HMRC before you take your main withdrawal. Your main withdrawal will then be taxed correctly from the outset.

Not all providers support this approach, so check with yours first.

Multiple Smaller Withdrawals

If you take regular income from your drawdown pot rather than a single large lump sum, your provider is more likely to have the correct tax code in place and tax you accurately from the second payment onwards. The first payment may still be on emergency tax, but the overpayment will be smaller.

Wait for HMRC to Update Your Code

If you're not in a hurry, your pension provider may receive an updated tax code from HMRC automatically through the PAYE system — particularly if you have other income sources. Once the correct code is applied, future withdrawals will be taxed accurately. However, this approach doesn't help with the tax already overpaid on your first withdrawal.

What If the Tax Year Has Already Ended?

If you overpaid tax in a previous tax year and didn't submit a reclaim form in time, you can still claim through your Self Assessment tax return (if you complete one) or by contacting HMRC directly to request a tax review. HMRC will generally process a refund for overpaid tax going back up to four years.

How This Fits Into Drawdown Planning

Emergency tax on pension withdrawals is one of several tax considerations that make drawdown more complex than it first appears. Others include:

- The Money Purchase Annual Allowance (MPAA): Triggering flexible access limits future pension contributions to £10,000 per year. See our guide: MPAA explained — the £10,000 trap.

- Income tax on withdrawals: Only 25% of your pension pot (the tax-free cash) is free of income tax. The remaining 75% is taxed as income in the year you take it.

- Sequence of returns risk: How much you withdraw — and when — has a significant impact on long-term sustainability. See: Sequence of returns risk in drawdown.

- Sustainable withdrawal rates: Many advisers recommend drawing no more than 3.5–4% of your pot per year to preserve capital over a 25–30 year retirement. See: Safe withdrawal rate in pension drawdown.

Getting the tax right from the outset — or reclaiming overpaid tax promptly — is an important part of making your drawdown income as efficient as possible.

Compare Pension Drawdown Providers

Charges, flexibility, and tax efficiency vary significantly between providers. Compare the leading UK drawdown providers side by side.

Compare Providers Now →Key Takeaways

- Emergency tax applies to your first flexible pension withdrawal because your provider doesn't hold an up-to-date tax code

- It taxes your withdrawal as if you earn that amount every month — leading to significant overpayment

- You can reclaim overpaid tax immediately using P55 (partial withdrawal), P53Z (full withdrawal + other income), or P50Z (full withdrawal + no other income)

- Online submissions are processed in 4–6 weeks; postal takes 8–12 weeks

- You may be able to avoid emergency tax by taking a small initial withdrawal first or switching to regular income payments

- Overpaid tax from previous tax years can be reclaimed via Self Assessment or by contacting HMRC directly

This article is for general information only and does not constitute financial advice. Tax rules are subject to change. Speak to a qualified financial adviser for guidance on your personal circumstances.

Further reading: Emergency Pension Tax: Avoid the Retirement Trap

The transition into retirement should be a period of celebration, yet for thousands of new retirees each year, the first experience of "Pension Freedom" is a financial cold shower. You plan a withdrawal to pay for a once-in-a-lifetime trip or home renovations, only to find that nearly half of your money has disappeared into the hands of HMRC before it even reaches your bank account.

This isn - t a permanent loss, but it is a significant "liquidity shock" known as Emergency Tax.

In the 2025/26 tax year, the issue remains a major hurdle. This guide explains why it happens, how the "Month 1" tax code works, and - most importantly - how you can legally avoid or quickly reclaim these funds.

1. The Retirement "Tax Trap": Why It Happens

When you reach age 55 (rising to 57 in 2028) and decide to access your defined contribution pension, you usually have the right to take 25% of your pot tax-free. The remaining 75% is treated as taxable income.

The problem arises because of how the UK - s PAYE (Pay As You Earn) system is designed. It is built for employees who receive a steady, predictable monthly salary. It is not built for retirees who might take a large, one-off "lump sum" to kickstart their retirement.

The "Month 1" (M1) Tax Code Explained

If your pension provider does not have a current, cumulative tax code for you (which is almost always the case for a first-time withdrawal), they are legally required by HMRC to apply an emergency tax code on a "Month 1" basis.

How the math works against you:

- HMRC sees your one-off withdrawal (say, £20,000).

- The system "assumes" you are going to receive this same amount every month for the rest of the tax year.

- It multiplies that £20,000 by 12, calculating your "annual income" as £240,000.

- It then applies the relevant tax bands (Basic, Higher, and Additional) as if you were a multi-millionaire, resulting in a massive over-deduction.

Example: If you withdraw £10,000 taxable income in Month 1 of the tax year, the system assumes an annual income of £120,000. You will only be granted 1/12th of your Personal Allowance for that specific payment, with the rest taxed at 20% and 40%.

2. How to Avoid Emergency Tax (Before You Withdraw)

While the system is rigid, there are tactical ways to ensure you aren't hit with the full weight of emergency tax.

Strategy A: The "Small First Withdrawal" Trick

This is the most effective way to "wake up" the HMRC system without losing a fortune.

- Withdraw a small amount first: Instead of taking your full desired lump sum, take a small taxable withdrawal (e.g., £100 or £500).

- Wait for the tax code: This small payment triggers a notification to HMRC. They will then issue a proper, cumulative tax code to your pension provider.

- Take the larger sum: Once your provider has the correct code (usually within 4 - 6 weeks), you can withdraw your main lump sum. Because the provider now has your "real" code, the tax deducted will be much closer to your actual liability.

Strategy B: Provide a P45

If you have recently stopped working, you will have been issued a P45 by your former employer. Give this to your pension provider before you make your first withdrawal.

- The P45 contains your total earnings and tax paid to date in the current tax year.

- While some providers may still use an emergency code for the very first payment, having a P45 significantly increases the chances of them applying the correct code immediately.

Strategy C: Tactical Timing

The UK tax year runs from April 6th to April 5th.

- If you take a lump sum in April (Month 1), you could be waiting nearly a year for an automatic refund if you don't proactively claim it.

- If you take the money in March (Month 12), the tax system is much closer to "reconciling" itself, and any overpayment is usually corrected automatically within a few weeks as the new tax year begins.

3. How to Reclaim Your Money: The "P-Forms"

If you have already been hit by emergency tax, do not wait for HMRC to notice. They will eventually reconcile your account at the end of the tax year, but this can take months. To get your refund within 30 days, you must use the correct HMRC form.

| Form | When to Use It |

|---|---|

| Form P55 | Use this if you have taken a partial withdrawal from your pension and you do not intend to take further regular payments this tax year. |

| Form P53Z | Use this if you have emptied your entire pension pot and you have other sources of income (like a job or other pensions). |

| Form P50Z | Use this if you have emptied your entire pension pot and you have no other income (other than potentially the State Pension). |

Where to find these forms?

You can complete these forms online via the GOV.UK website or through your Personal Tax Account. Using the digital service is significantly faster than posting a paper form.

4. Current Tax Rates and Allowances (2025/26)

To understand how much you should be paying, keep these thresholds for the 2025/26 tax year in mind:

- Personal Allowance: £12,570 (This is the amount you can earn tax-free).

- Basic Rate (20%): On income between £12,571 and £50,270.

- Higher Rate (40%): On income between £50,271 and £125,140.

- Additional Rate (45%): On income over £125,140.

(Note: Rates in Scotland differ slightly, with more granular bands ranging from 19% to 48%)

5. Checklists for Retirees

To ensure a smooth withdrawal, follow this step-by-step process:

- Check with your provider: Ask them specifically which tax code they will use for your first withdrawal.

- Verify your Personal Tax Account: Log in to the HMRC portal to ensure your income details for the year are up to date.

- Calculate the "Net" amount: If you need £20,000 for a specific purchase, remember that an emergency tax deduction might leave you with only £14,000. You may need to "gross up" your withdrawal or use the "Small First Withdrawal" trick mentioned above.

- Keep your P45 safe: It is the most valuable document you have when transitioning from work to retirement.

Summary

Emergency tax is an administrative byproduct of a system designed for the 20th-century workforce, not the flexible 21st-century retiree. While it can feel like a "theft" of your hard-earned savings, it is merely a temporary overpayment.

By using a small "test" withdrawal, providing your P45, or being ready with a P55 form the moment the money hits your account, you can minimize the time your money spends sitting in HMRC - s coffers.

Further reading: Emergency Tax on Pension Withdrawals: What You Need to Know

Why Is My First Pension Withdrawal Taxed So Heavily?

If you've recently taken your first withdrawal from a pension in drawdown and found the tax deducted was much higher than expected, you're not alone. This is one of the most common complaints among people accessing their pension for the first time, and it's down to something called emergency tax.

Emergency tax is a temporary measure used by pension providers when they don't have your correct tax code. The good news is that any overpaid tax can be reclaimed - but understanding why this happens can help you plan ahead and avoid nasty surprises.

How Does Emergency Tax Work?

When you take money from your pension, your provider must deduct income tax under PAYE (Pay As You Earn). However, unlike your employer, pension providers often don't have your tax code when you first access your pension.

Without a proper tax code, providers use what's known as an emergency tax code. This code assumes you'll be making the same withdrawal every month for the rest of the tax year. If you're taking a one-off lump sum, this can result in a significant over-deduction of tax.

Example of Emergency Tax in Action

Consider this scenario: Sarah takes a one-off withdrawal of £20,000 from her pension (after her 25% tax-free lump sum). Under emergency tax rules, the provider might assume she'll take £20,000 every month - that's £240,000 for the year.

This pushes her into higher tax bands, resulting in much more tax being deducted than she actually owes. If she's only taking this single withdrawal and has no other income, her actual tax bill would be much lower.

Emergency Tax Codes Explained

There are three main types of emergency tax codes you might encounter:

- 0T (cumulative) - No tax-free personal allowance is given, and tax is calculated cumulatively based on earnings so far in the tax year

- 0T W1/M1 (week 1/month 1) - No personal allowance, and tax is calculated as if this is your only income for that period, multiplied to estimate the full year

- BR (basic rate) - All income taxed at 20% with no personal allowance

The 'W1' or 'M1' suffix indicates a non-cumulative or 'week 1/month 1' basis, meaning your previous earnings that tax year aren't considered. This often leads to the highest over-deductions.

Who Is Most Affected?

Emergency tax particularly affects people in these situations:

- Those taking their first pension withdrawal

- People taking large one-off lump sums

- Those who have recently retired and no longer have employment income

- Anyone accessing a pension from a provider they haven't used before

- People making withdrawals early in the tax year (April/May)

If you're still working and your employer has already used your personal allowance, emergency tax may actually be closer to correct - but even then, the calculation method can cause issues.

How Much Tax Should You Actually Pay?

Understanding the standard income tax rates can help you estimate what you should owe. For the 2025/26 tax year, the rates are:

- Personal Allowance: £0 - £12,570 (0% tax)

- Basic Rate: £12,571 - £50,270 (20% tax)

- Higher Rate: £50,271 - £125,140 (40% tax)

- Additional Rate: Over £125,140 (45% tax)

Note that the personal allowance reduces by £1 for every £2 of income above £100,000, disappearing entirely at £125,140.

Your pension withdrawal is added to any other income you have that year (employment, state pension, rental income, etc.) to determine which tax bands apply.

How to Avoid Emergency Tax

While emergency tax can't always be avoided, there are steps that may help:

1. Take a Small Initial Withdrawal

Some people take a small first withdrawal (perhaps just a few hundred pounds) to trigger the tax code process. Once HMRC issues your correct code to the provider, subsequent withdrawals should be taxed correctly. This approach typically takes 30-60 days to resolve.

2. Provide Your P45

If you've recently stopped working, providing your P45 to your pension provider can help them apply the correct tax code from the start.

3. Time Your Withdrawals

Taking withdrawals later in the tax year gives HMRC more time to issue correct tax codes to providers. Withdrawals made in March may face fewer emergency tax issues than those in April or May.

4. Spread Withdrawals Across Tax Years

Taking smaller withdrawals across multiple tax years can keep you in lower tax bands overall, reducing both actual tax and potential emergency tax issues.

How to Claim Back Overpaid Tax

If you've had emergency tax deducted, you have several options to reclaim it:

Option 1: Wait for Automatic Correction

HMRC will eventually receive information about your pension withdrawal and recalculate your tax. If you've overpaid, they'll typically issue a refund automatically - but this can take until after the end of the tax year.

Option 2: Complete an HMRC Form

For faster repayment, HMRC provides specific forms depending on your situation:

- P50Z: If you've withdrawn all your pension and have no other income

- P53Z: If you've withdrawn all your pension but have other taxable income

- P55: If you've taken only part of your pension

These forms are available on the HMRC website and can be submitted online or by post. Claims are typically processed within 30 days.

Option 3: Self Assessment

If you complete a Self Assessment tax return, any overpaid tax will be calculated and refunded through that process. This is automatic but means waiting until you file your return.

What Information Will You Need?

To claim a tax refund, you'll typically need:

- Your National Insurance number

- Details of the pension withdrawal (amount, date, tax deducted)

- A P45 from your pension provider (usually provided after withdrawal)

- Details of any other income in the tax year

- Your bank details for the refund

Keep all documentation from your pension provider as this will be needed for any claim.

Planning Ahead

Emergency tax is frustrating, but it's a temporary administrative issue rather than a permanent tax increase. The key points to remember:

- Any overpaid tax will be refunded - you won't lose money permanently

- Using HMRC forms speeds up the refund process significantly

- Small initial withdrawals can help establish correct tax codes

- Timing and spreading withdrawals can reduce the issue

- Your actual tax liability depends on your total income for the year

> Try our free Pension Drawdown Calculator to model different withdrawal scenarios and see how long your pension could last.

When to Seek Professional Advice

While emergency tax itself is straightforward, pension withdrawals interact with various aspects of your financial situation. Tax efficiency, withdrawal sequencing, and long-term sustainability all benefit from proper planning.

If you're uncertain about the most tax-efficient way to access your pension, or if you have complex income sources, speaking to a qualified financial adviser can help you develop a strategy that minimises tax over your retirement, not just on a single withdrawal.

Use our pension drawdown calculator to plan your withdrawals, and compare drawdown providers to find the best platform for your needs.

This article is for information purposes only and does not constitute financial advice. Tax rules can change, and individual circumstances vary. Always consult a qualified financial adviser for guidance specific to your situation.